WHEN A BEAUTIFUL DELEVERAGING TURNS UGLY

Special Report

September 30, 2015

It is necessary to

understand how the economy works in order to develop a perspective on

the financial markets both in the short-run as well as the long-term.

Ray Dalio, one of the best macro thinkers of our generation and

founder of Bridgewater, the largest hedge fund in the world, has created

a framework to explain the dynamics of an economy.

In this discussion, I

am going to use Dalio’s framework of the economy to offer a perspective

on how we may be at one of the most significant junctures in the last 85

years as it relates to the global economy and implications for the

financial markets. In order

for this perspective to make sense, you first need to understand Dalio’s

framework. He has created a

short, thirty minute video which is a good depiction of how the economy

functions. Instead of

explaining it here, it is much more effective for you to do a Google

search for “How The Economic Machine Works” by Ray Dalio and watch the

video yourself. The video

can be seen at

www.economicprinciples.org or you can also search for it on YouTube.

So, I encourage you to stop reading, watch the video and then

return to this discussion.

Now that you have seen

Dalio’s video, let’s use that framework to think through a possible

scenario that may unfold in the economy and the financial markets.

To do this, I will first review a few key dynamics from the

video. Then, I will use his

framework to offer a perspective on the current situation and a scenario

that may be on the verge of unfolding.

In addition, I will put that scenario within the context of the

global environment. At the

end, I will provide a few concluding remarks.

Let’s get started.

POINTS OF EMPHASIS REGARDING

“THE ECONOMIC MACHINE”…

In Dalio’s description

of The Economic Machine, productivity drives the long-term trend in

economic growth by the participants working either harder or smarter.

Then, credit cycles either accelerate growth by pulling demand

forward during credit expansions or slow down growth when credit

contracts and repayments increase.

These credit cycles cause economic growth to oscillate above and

below the longer-term trend.

Also, there is a short-term credit cycle that last usually

between 5 and 8 years and a long-term credit cycle that typically occurs

over a 75 to 100 year period.

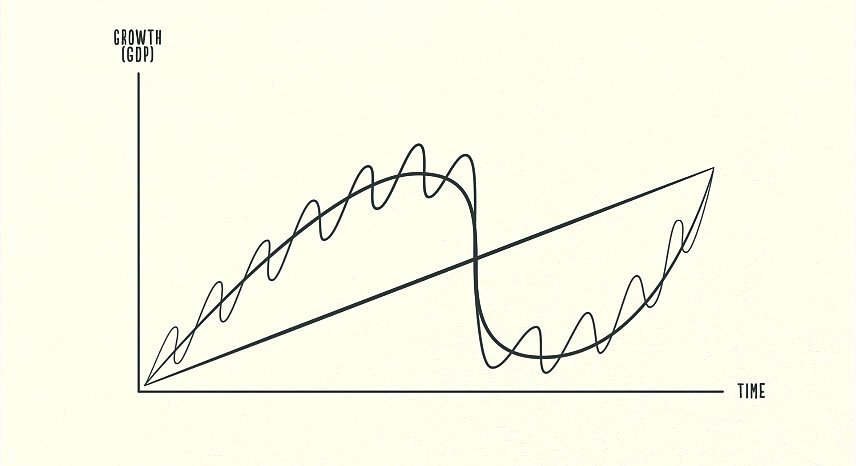

To provide a visual on

how the short-term and long-term debt cycles oscillate around the

productivity trend of fundamental growth, here is the chart Dalio used

in his video.

In the chart above, the

straight line going higher over time is the productivity line which

drives long-term economic growth.

The larger wave is the long-term debt cycle and the smaller wave

reflects the short-term credit cycle.

The short-term cycles trend higher as human nature drives

consumption levels higher than income levels until an economy reaches an

unsustainable amount of debt accumulation.

The long-term cycle begins at low levels of debt in the economy

and ends at very high levels of debt.

And, the process of returning from the peak in the long-term

cycle back to low amounts of debt is called a deleveraging.

During these credit

cycles, the central bank plays an active role as we have all seen.

In the short-term cycle, the central bank uses interest rates to

influence either the acceleration or deceleration of credit growth.

When credit growth is accelerating quickly and inflation concerns

begin to surface, the central bank raises rates to make the cost of

credit more expensive so as to temper growth.

On the other side, when credit growth is slowing or contracting

during a recession, the central bank lowers rates to make credit less

expensive to try to increase spending and reignite growth.

This goes on for decades until an economy is saturated in debt.

Then, there is a

tipping point where a deleveraging occurs and even though the central

bank lowers rates, it has little effect because participants in the

economy cannot or will not take on new debt regardless of how cheap it

is. The long-term credit

expansion is a self-reinforcing cycle of growth and a deleveraging feeds

off itself as well but in a downward cycle.

Often, central banks are at or near zero interest rates during

deleveragings.

During deleveragings

people cut their spending, debt is reduced through defaults and

restructurings, wealth is redistributed through tax policies and the

central bank prints money.

While inflation is the primary concern of central banks during the

long-term credit expansion part of the cycle, fears shift to deflation

in the deleveraging period of the cycle.

With this in mind, let’s now shift to putting the current

environment within the context of Dalio’s Economic Machine framework.

SO, WHERE ARE WE NOW???

Debt cycles are a key

driver of the overall machine so let’s begin by taking a look at debt

levels as a percent of GDP over the last 100 years.

Here is a chart from Gamco Mathers Fund.

If you look at the

chart above, you can see the prior peak in the long-term debt cycle in

the 1930’s and the subsequent deleveraging.

The debt levels were reduced back to a low level which then reset

the economic foundation for the next long-term cycle of debt

accumulation. Now, if you

look at the end of the chart, you see potentially another peak which was

around 2007, and happens to be about 75 years from the last peak.

After the recent peak,

we saw the first wave of deleveraging in 2008 and 2009.

And, what have we seen from the central bank; move to the zero

bound in interest rates and the printing of over $4 trillion in new

money [the chart embedded at the top center above puts how much money we

have printed into context].

The last time we saw anything close to these extreme monetary policies

was in the Great Depression.

These are not policies found during the uptrend period of the

long-term debt cycle.

AN EMERGING SCENARIO…

Now, here is where it

gets even more interesting and these are my interpretations and I have

not heard Dalio’s perspective on this.

So, as Dalio describes, the short-term credit cycle oscillates

around the long-term debt cycle trend, as shown in the first chart

earlier. To dive deeper

into the current environment, let’s magnify the chart of both short and

long-term debt cycles of the recent period.

In the chart above, the

black line represents the long-term debt cycle and the red line

represents the short-term debt cycle.

So, here is the scenario.

The peak in both the short and long-term debt cycles occurred in

2007. Period # 1 above

shows that the short-term debt cycle accelerated downward at the same

time the long-term debt cycle began to roll over.

When the short-term and long-term cycles line up, you get

acceleration in the overall trend, both on the upside and on the

downside.

THE FIRST WAVE…

In this first wave

down, we had the Great Recession and a financial crisis which led to a

shift in monetary policies back to the Great Depression era with the

central bank cutting rates to zero and starting up the printing press as

fears of deflation surfaced.

Bernanke just happened to be the chair of the central bank and

his field of academic study was focused on the Great Depression; and he

pulled out the playbook.

During this wave #1 in the chart above, we also saw high profile

bailouts of failed institutions, increased government guarantees in

certain areas of the financial system, as well as significant debt

restructurings. These

dynamics are picture perfect for what is found in a deleveraging.

These extreme monetary

policies and government actions had the effect of slowing down the

deleveraging process and turning it back up, but at a slower ascent,

from 2009 through 2015, which is period # 2 above.

The initial descent and subsequent reprieve from the downward

deleveraging force of the long-term cycle has played out in the form of

another short-term credit cycle.

THE SECOND WAVE…

Over the past six years

or so since 2009, the short-term credit cycle turned back up in the

midst of the long-term cycle being down.

Instead of good economic growth, we have seen very muted growth

and one of the worst “recoveries” on record.

When the cycles are going against one-another in the long-term up

cycle, you get a mild to moderate recession and when the cycles are

going against one-another in the long-term down cycle, you get a mild

recovery. This mild

economic recovery occurred during period # 2 in the chart above.

This initial wave of

the deleveraging process was met by unprecedented monetary policies.

That has created this battle between the deflationary forces of

deleveraging and the inflationary forces of the monetary policies.

Dalio’s Economic Machine outlines what he calls a “Beautiful

Deleveraging” when the central bank finds the right balance of monetary

policy so that the deflationary pressures are balanced by the

inflationary policies. If

the balance is managed appropriately, it enables the economy to

deleverage and reset debt levels without too much pain or causing a

depression. Through periods

# 1 and # 2 above, it might appear based on this framework that the

deleveraging has been “beautiful” so far.

However, the

significant challenge is that if you look back up at the total debt

chart, you can see that the deleveraging of the long-term debt has only

begun here in the U.S. and there is a whole lot left to go.

And, to accomplish this “beautiful” deleveraging so far, the

central bank has already used much of its available ammunition.

Instead of allowing the

deleveraging to occur, our central bank has created a short-term

reflation of debt. That

implies that our central bank used too much force in the first wave down

instead of achieving the desired balance of monetary policy.

The deleveraging cycle will continue and the perceived benefits

of the monetary policies are subsiding.

Now, if we look at the

possibility that the short-term credit cycle is peaking once again in

the midst of the long-term cycle continuing downward, we could see

another serious economic contraction which would have significant

implications for financial markets as well as monetary policy.

By the way, the time between the ’07 peak and a ’15 peak in the

short-term cycle would be 8 years which fits the typical range for the

short-term cycle outlined by Dalio.

Before I discuss the

impact of the cycles converging again, let’s step back for a moment and

consider the global environment.

THE GLOBE IS AWASH IN DEBT…

Since the potential

recent peak in the long-term debt cycle here in the U.S. back in 2007,

global debt has continued to increase at an alarming rate.

McKinsey & Company, the leading global consulting firm, recently

published a study in February of this year called “Debt and (Not Much)

Deleveraging. I will quote

some of their findings here.

“Seven years after the

bursting of a global credit bubble resulted in the worst financial

crisis since the Great Depression, debt continues to grow.

In fact, rather than reducing indebtedness, or deleveraging, all

major economies today have higher levels of borrowing relative to GDP

than they did in 2007. Global

debt in these years has grown by $57 trillion, raising the ratio of debt

to GDP by 17 percentage points (Exhibit 1).

That poses new risks to

financial stability and may undermine global economic growth.”

“In our study, we

pinpoint three areas of emerging risk: the rise of government debt,

which in some countries has reached such high levels that new ways will

be needed to reduce it; the continued rise in household debt—and housing

prices—to new peaks in Northern Europe and some Asian countries; and the

quadrupling of China’s debt, fueled by real estate and shadow banking,

in just seven years.”

“Government debt is

unsustainably high in some countries.

Since 2007, government debt has grown by $25 trillion.

It will continue to rise in many countries, given current

economic fundamentals. Some

of this debt, incurred with the encouragement of world leaders to

finance bailouts and stimulus programs, stems from the crisis. Debt also

rose as a result of the recession and the weak recovery.

For six of the most highly indebted countries, starting the

process of deleveraging would require implausibly large increases in

real-GDP growth or extremely deep fiscal adjustments.

To reduce government debt, countries may need to consider new

approaches, such as more extensive asset sales, one-time taxes on

wealth, and more efficient debt-restructuring programs.”

“Household debt is

reaching new peaks. Only in

the core crisis countries—Ireland, Spain, the United Kingdom, and the

United States—have households deleveraged.

In many others, household debt-to-income ratios have continued to

rise. They exceed the peak

levels in the crisis countries before 2008 in some cases, including such

advanced economies as Australia, Canada, Denmark, Sweden, and the

Netherlands, as well as Malaysia, South Korea, and Thailand.”

“Fueled by real estate

and shadow banking, China’s total debt has nearly quadrupled, rising to

$28 trillion by mid-2014, from $7 trillion in 2007.

At 282 percent of GDP, China’s

debt as a share of GDP, while manageable, is larger than that of the

United States or Germany. Three

developments are potentially worrisome: half of all loans are linked,

directly or indirectly, to China’s overheated real-estate market;

unregulated shadow banking accounts for nearly half of new lending; and

the debt of many local governments is probably unsustainable.”

McKinsey’s study raises

questions about how much, if any, has the U.S. really deleveraged since

2007. Households have

deleveraged some but the government has added new debt.

Also, it is not unusual to see debt actually go up in the

government sector during the initial phases of a deleveraging as they

spend to try to maintain growth, while tax receipts fluctuate lower.

In summary, their study shows that the world is awash in debt.

Now, if we look at the

three largest developed economies as the U.S., Europe, and Japan it is

interesting to note what we have seen from a monetary policy standpoint.

Each is already at or near the zero bound in interest rate policy

and each has printed significant amounts of money over the past few

years. Some countries

within Europe have even gone the extra step of moving to negative rates.

These are deleveraging and Great Depression-type policy measures

which match up well with the scenario that the world economies are

either in or moving toward the deleveraging part of their long-term debt

cycles.

THE THIRD WAVE…

Next, let’s turn back

to the potential scenario that the short-term and long-term credit

cycles may be on the verge of lining up in the same direction here in

the U.S. once again. In the

earlier chart showing the long-term cycle with the black line and the

short-term cycle with the red line, this would mean that we are moving

toward the wave down in period # 3.

Then, the question

comes to whether our central bank used up too much of its ammunition in

the first wave down of the deleveraging cycle.

It is debatable what effects those policies have had on the real

economy but what we do know is that it has inflated asset prices back up

to very lofty levels from a valuation perspective.

It appears so far that the deflation pressures from the

beginnings of the deleveraging cycle have continued to manifest itself

in the real economy while the inflationary pushes from the monetary

policies have been reflected in the financial markets with the

levitation of asset prices.

If we are moving into

that third period on the chart, monetary policy is likely to go even

further out on the spectrum which would first include a new round of

money printing or, QE 4. Other

types of asset purchases will likely be included as the central bank

looks for more direct ways to push money into the system.

Also, negative interest rates would likely follow and we even had

one central bank member mention that possibility at the latest meeting.

Fiscal policy will look for new ways to get involved as well.

This period would include the next economic contraction and a

high probability that asset prices would reconnect to fundamentals.

Each incremental step in monetary policy over the past few years

has been shown to be less effective and when you are already at extremes

the perceived benefit will likely diminish even further.

If the central bank

used up too much ammunition in the first phase of the deleveraging and

the next frontier of monetary policy is perceived as being ineffective

at a time when the short and long-term cycles converge once again, that

is the point when the previous “beautiful” deleveraging turns ugly.

A SYCHRONOUS GLOBAL

DELEVERAGING…

Now, overlay what is

going on around the world and the potential for a global synchronous

deleveraging at a time when the world central banks are already at

extreme policies, the scenario turns even more interesting.

If we have the short-term credit cycles turn back down and

reconnect with the long-term debt deleveraging cycles around the globe

at the same time, the deflationary forces will be powerful relative to

any conceptual monetary strategy.

The implications for stocks, bonds, currencies, commodities and

other assets become tricky as all central banks would likely end up

printing the money required for the debts that do not end up in default

or restructured along the way.

How that money infiltrates into the economic system and financial

markets is something to think through as one positions around this

scenario. Social

implications will be notable as well.

Let’s conclude this

discussion. Ray Dalio’s

Economic Machine framework for understanding how the economy works is

one of the best depictions available.

Overlaying that framework on the U.S. and global economies with a

historical perspective, helps one to understand potential scenarios that

may unfold as this deleveraging process continues.

It is hard to imagine scenarios such as the one described here in

the midst of daily activities and the extreme short-term focus in the

financial markets by participants. However,

in 2007 most all did not imagine what would occur in the first phase of

the deleveraging during 2008 and the subsequent monetary policies that

followed. It is a time to

at least consider a scenario such as this since the implications are

significant and ensure you have a plan to position appropriately.

Joseph R. Gregory, Jr.